Prediction markets are evolving from simple betting platforms into full-blown financial infrastructure. Paradigm’s paper on Multiverse Finance formalizes a vision where the financial system splits into parallel universes, each pricing what assets would be worth under a specific future state of the world.

This isn’t science fiction. The core primitive — conditional tokens — already exists and processes billions in volume through platforms like Polymarket. But Paradigm’s vision requires infrastructure that doesn’t exist yet: a way to borrow and lend across those parallel worlds. The financial plumbing to make conditional tokens truly composable — lending, leverage, and capital-efficient collateral. That’s the gap Varla fills.

From Prediction Markets to Parallel Universes

The idea starts simply. Consider a prediction market on whether Jerome

Powell will be fired in 2025. You can buy a notFiredUSD token

for 89 cents that pays $1 if he isn’t fired. But that capital is locked —

you can’t use it as collateral anywhere because if Powell were suddenly

fired, the token’s value could drop to zero faster than any system could

liquidate your debt.

Dave White’s key insight changes this calculus entirely: there is no

problem when using notFiredUSD as collateral to borrow

notFiredETH. If Powell is fired, both your collateral and

the asset you borrowed become worthless simultaneously. No liquidation

issue. No flash-crash risk. The existential risk is perfectly correlated.

What Are Verses?

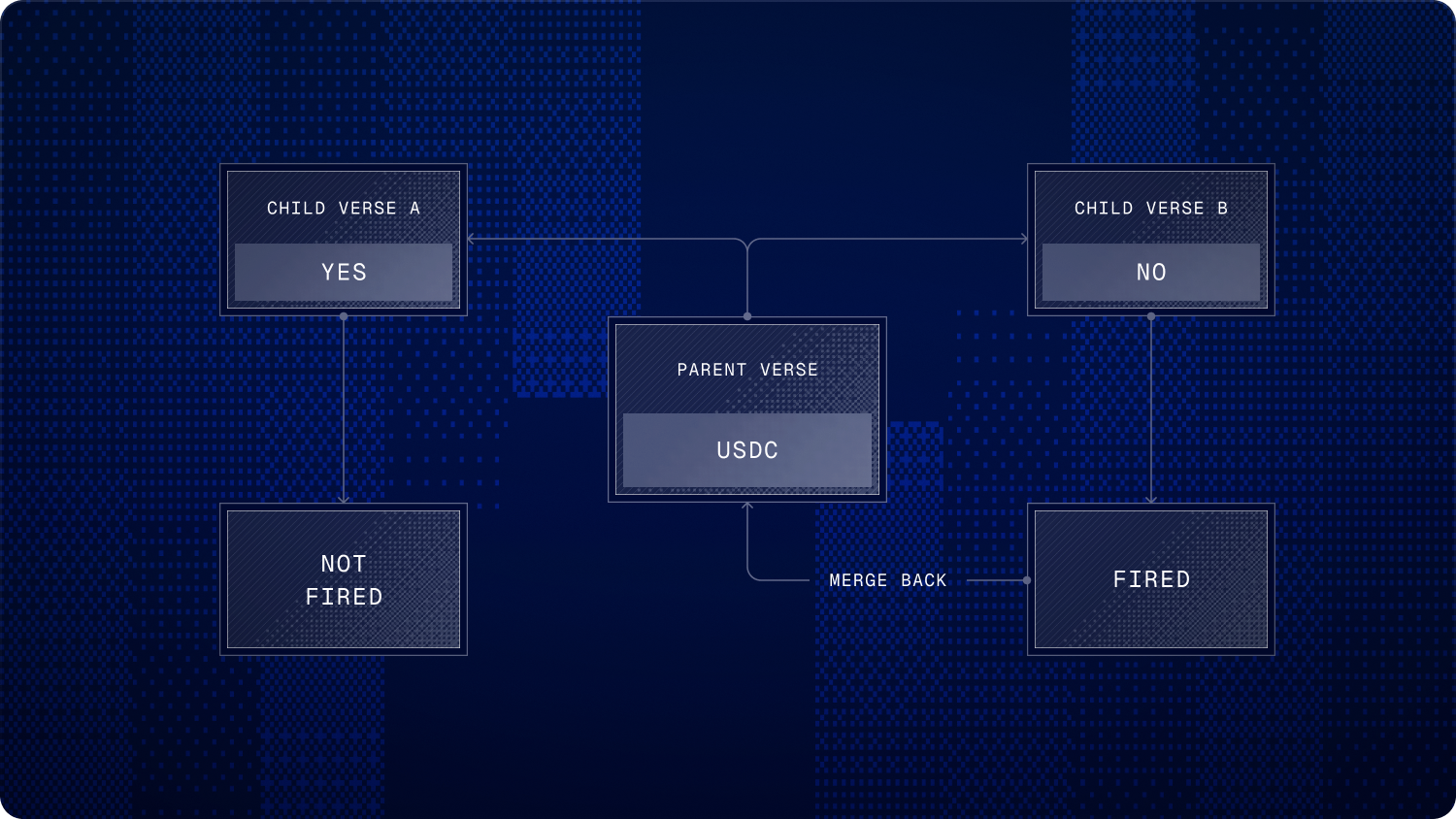

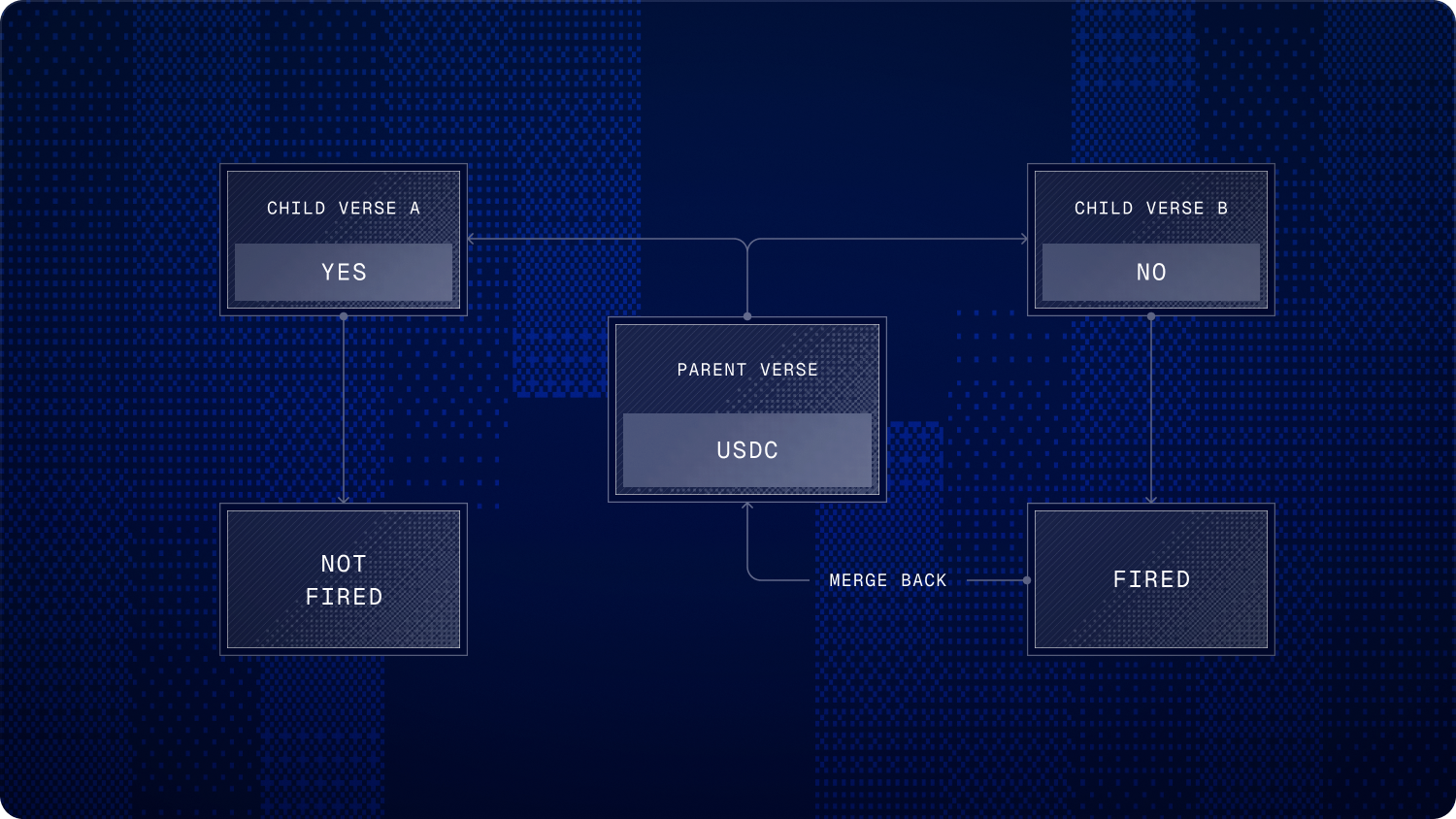

The paper formalizes this through “verses” — parallel financial environments scoped to a specific outcome. A verse is mathematically an event in probability theory: a set of possible states of the world. Every verse has a complement (fired vs. not-fired), verses can be combined through unions and intersections, and today’s universe is the parent verse that contains all possible outcomes.

The mechanism is elegant. If you own 1 unit of token T in a parent verse, you can push down your ownership to a partition — giving up your token in the parent verse and receiving 1 unit in each child verse. This is exactly how Gnosis Conditional Tokens work: take $1 and mint one YES and one NO token. Conversely, holding 1 unit in every child verse lets you pull up back to the parent — merge YES + NO back into $1.

When a verse resolves, the losing branches disappear along with all their state. The winning branch becomes a complete partition of the parent, and you can pull your assets back up to reality.

Why Lending Is the Missing Layer

The paper explicitly states that the simplest version of Multiverse Finance “could be implemented today on mainnet by allowing conditional tokens for the same outcomes to be borrowed and lent against each other on an Aave-like protocol.” The full vision goes further — complete financial ecosystems within each verse, with lending, derivatives, AMMs, and yield farming — all scoped to a specific future state of the world.

But even before we reach intra-verse composability, there’s an enormous opportunity in cross-verse lending: using conditional tokens from child verses as collateral to borrow assets from the parent verse. This is lending against prediction market positions — borrowing USDC against your Polymarket holdings.

Cross-verse lending is harder than intra-verse lending because the collateral can go to zero while the borrowed asset retains value. This is precisely why it requires purpose-built infrastructure: conservative pricing oracles, tiered risk parameters, and carefully designed liquidation mechanisms.

How Varla Implements This Today

Varla is a lending protocol purpose-built for conditional tokens. Here’s how its architecture maps to the Multiverse Finance framework:

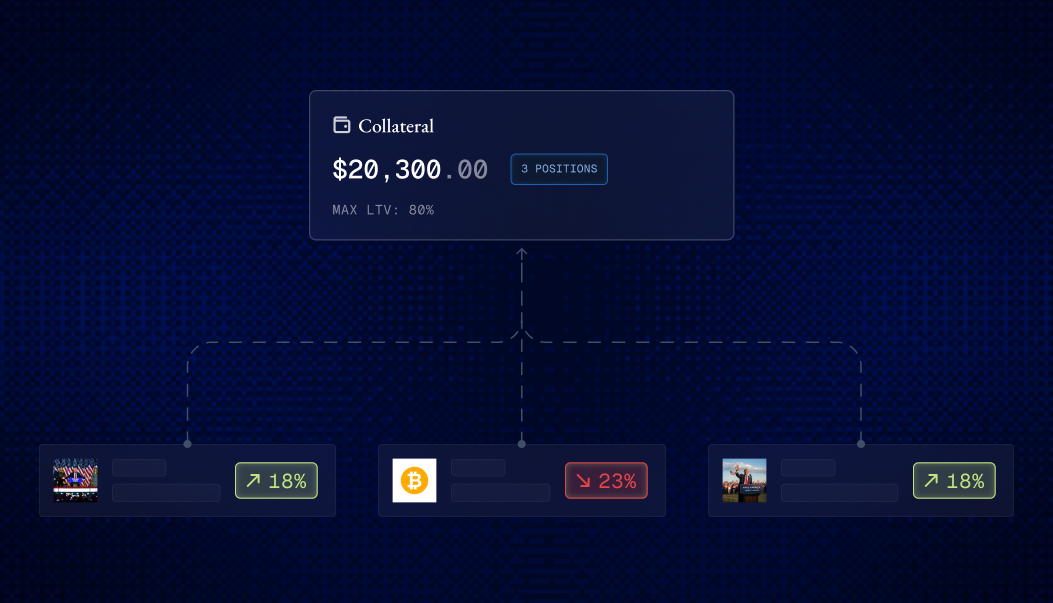

The protocol manages cross-margin accounts where multiple prediction market positions serve as combined collateral. Rather than each position being siloed, your entire portfolio contributes to your borrowing power — reducing the capital fragmentation that the Paradigm paper identifies as the key bottleneck for conditional markets.

Not all conditional tokens carry equal risk. Varla assigns risk tiers (Conservative at 80%, Moderate at 65%, Risk at 50%) with optional per-position overrides. This maps to the intuition that some verses are more “stable” than others — a market resolving in two years carries different risk than one resolving next week.

The oracle is purpose-built for thin prediction markets. It uses a push-based model that returns the minimum of spot price and TWAP for manipulation resistance, tracks staleness and liquidity validity, and applies low-liquidity LTV decay to automatically reduce exposure when market depth deteriorates. As a market approaches resolution — as the verse boundary thins and the probability of a sudden collapse increases — a linear LTV decay factor automatically reduces borrowing capacity in the final days before settlement.

The Liquidity Question

The paper contains a telling parenthetical that does a lot of heavy lifting: it envisions complete financial ecosystems within each verse, “liquidity issues aside.”

This qualifier is worth unpacking because it reveals the central tension in Multiverse Finance. In today’s financial system, there’s one version of USDC, one Uniswap ETH/USDC pool, one Aave USDC market. All liquidity is concentrated. In a fully realized multiverse, every verse needs its own copy of every financial primitive — its own lending pool, its own AMM, its own yield opportunities.

For N independent binary markets, there are 2^N possible verse intersections. Each needs its own liquidity. The combinatorial explosion makes full multiverse coverage impossible — there simply isn’t enough capital.

Even for a single market: if you deploy a lending pool for the “Powell Not

Fired” verse, an LP depositing notFiredUSD is making a conditional bet.

They only earn yield — and get their principal back — if Powell isn’t fired.

That’s a much harder sell than “deposit USDC, earn 5% APY unconditionally.”

The pool of willing LPs shrinks, utilization spikes, and borrow rates become

punitive.

The push-down / pull-up mechanism helps capital flow — a user can split $1

into firedUSD + notFiredUSD — but they’re now exposed to both verses

simultaneously. Capital doesn’t multiply when you split; it fragments.

This isn’t a flaw in the paper’s vision. It’s an honest constraint that any implementation must address. And it reshapes how we think about building multiverse infrastructure.

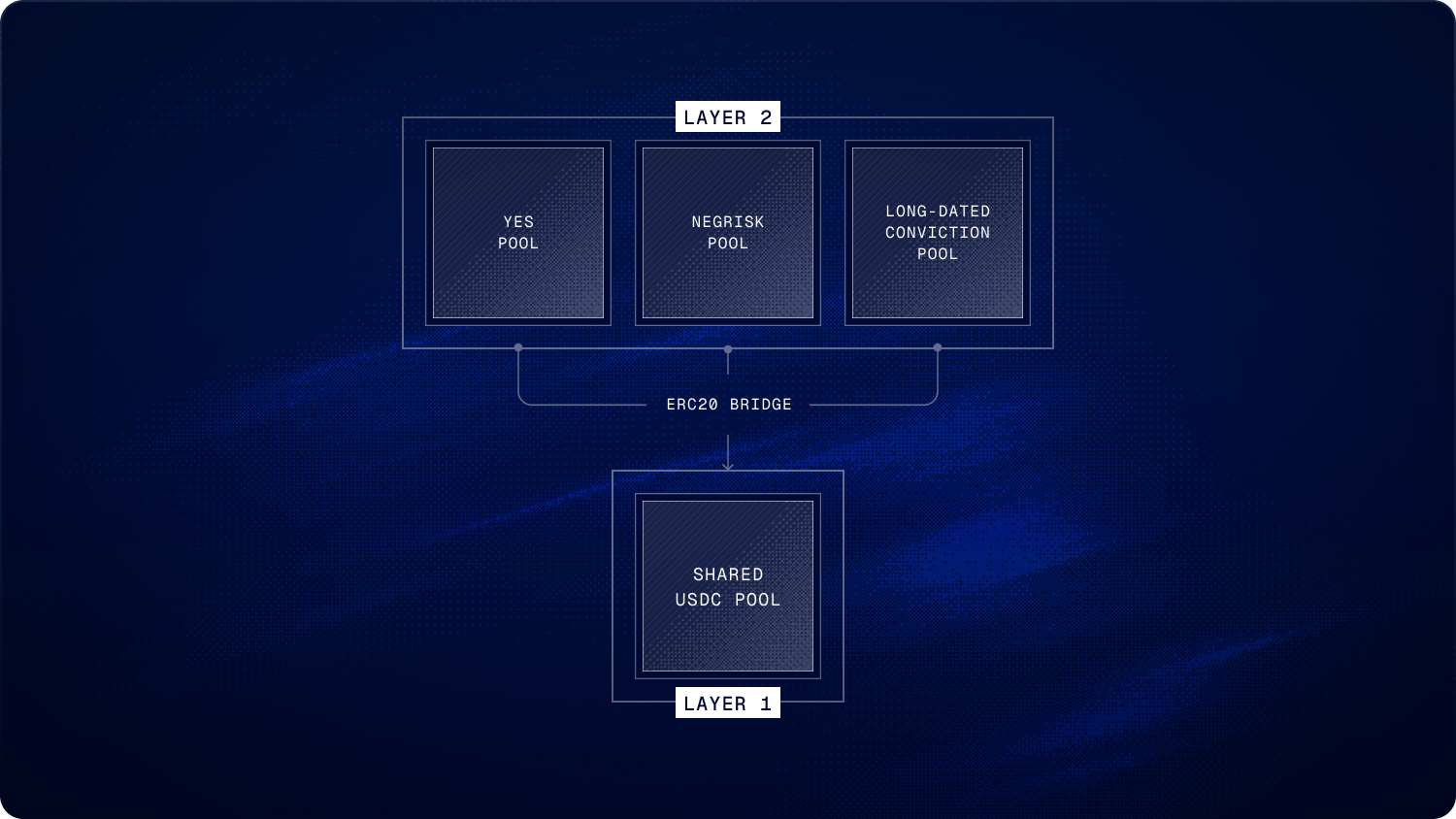

Two Layers of Multiverse Lending

Rather than a stepping-stone toward full per-verse financial ecosystems, we see Varla’s architecture as defining two complementary layers of multiverse lending:

Layer 1: Unconditional lending (the parent verse). This is Varla today — a single USDC pool where LPs earn yield regardless of which verses survive. Borrowers deposit conditional tokens as collateral and borrow unconditional stablecoins. All liquidity is concentrated. Risk is managed by the protocol through tiered LTV, oracle guards, and permissionless liquidation.

In the language of the paper, this IS the Multiverse Map for the “full universe” verse — the parent that contains all possible outcomes. It’s not a compromise; it’s the most capital-efficient configuration for the common case.

Layer 2: Verse-specific lending (targeted use cases). For specific high-value scenarios, verse-scoped pools make sense despite the fragmentation cost:

-

Leveraged prediction positions. A trader who wants 5x YES exposure can deposit YES tokens into a verse-scoped pool, borrow more YES, sell for USDC, and buy more YES. This leverage loop is impossible with unconditional lending alone and creates organic demand for verse-specific liquidity.

-

NegRisk market lending. Multi-outcome markets like “Who will be president?” have 5–10 outcome tokens all conditioned on the same event. These tokens have natural lending demand against each other — one pool per negRisk market, not per binary outcome, keeps fragmentation manageable.

-

High-conviction, long-dated markets. Markets with 6–12+ months to resolution and deep liquidity, where LPs already hold the conditional position and verse-specific yield is additive to an existing bet.

The bridge between these layers is straightforward: a thin fungible wrapper around a specific conditional token, which lets the existing vault accept conditional tokens as the lending asset without any pool-level changes. The wrapper is 1:1 backed and reuses the same pattern Polymarket already uses for negRisk wrapped collateral.

Varla’s architecture is designed to support both layers. The oracle already tracks condition IDs, resolution times, and opposite position pairs. The cross-margin engine supports multiple positions with per-position risk parameters. And the adapter pattern — live on Polymarket (Polygon), with Opinion Protocol (BSC) next — means new conditional token platforms and verse-scoped pools can be integrated without rebuilding the lending stack.

The Bigger Picture

The infrastructure to split financial reality into parallel branches already exists. Polymarket processes billions in monthly volume. MetaDAO is running real governance through conditional markets. Lightcone is building per-asset conditional tokens on Solana. What’s been missing is the financial plumbing to make those branches productive.

Lending is the foundation of that plumbing. It turns a static bet into dynamic capital. It lets a trader hold a conviction and simultaneously deploy that capital elsewhere. And it’s what ultimately enables the composable, verse-scoped financial ecosystems that Multiverse Finance envisions.