Something is converging. Polymarket sits on $450 million in open interest — capital that earns no yield, can’t be used as margin, and can’t offset risk anywhere. Hyperliquid is building HIP-4 to bring outcome trading natively into its margin engine. And Varla is live on Polygon mainnet, lending against Polymarket positions — with BSC support built and ready to ship.

Multiple layers of infrastructure are emerging around the same thesis: prediction market capital needs to stop sitting idle.

We traced wallet behavior across roughly 15,000 top prediction market traders and the pattern is consistent. The most sophisticated participants are running leveraged perpetual books with one hand while their prediction capital sits completely idle with the other. More than half of Polymarket’s open interest won’t resolve for 30 days or more. $155 million is locked for over a year. That’s not forgotten money — it’s fresh conviction capital, doing nothing.

$450 Million Doing Nothing

Nearly a fifth of the highest-volume prediction market wallets are simultaneously very active on Hyperliquid. These aren’t memecoin degens. Their perpetual books are almost perfectly balanced: 54% long, 46% short. They trade BTC, ETH, blue chips. They deploy around $29 million in margin and run an average leverage of 7x.

On prediction markets, they sit in long-dated election or Fed bets for months. On Hyperliquid, they hedge and manage risk. Two books, two platforms, two separate pools of capital.

The cost of this split: roughly $18 million in open prediction market positions that can’t be used as perpetual margin. At 7x leverage, that’s $128 million in trades they’re not making. Locked for a median of 32 days. Not some forgotten bag — fresh capital, doing absolutely nothing, while they’re running leveraged books on the platform next door.

Every dollar of prediction market capital that sits idle is a dollar that could be earning yield, backing a trade, or collateralizing a loan. Multiply that across the full $450 million in open interest and you start to see the scale of the opportunity.

Two Layers of Capital Efficiency

Capital efficiency in prediction markets isn’t a single problem with a single solution. It’s a stack — and different layers of that stack serve different functions.

Exchange-level infrastructure handles matching, settlement, and margin. This is what Hyperliquid builds at the HyperCore level. When outcome contracts live natively inside the matching engine alongside perpetuals and spot, portfolio margin can net correlated positions into one account. The exchange is the settlement layer.

Protocol-level infrastructure handles lending, yield generation, and cross-platform composability. This is what DeFi protocols add on top of exchanges — the same way Aave and Compound operate on top of Ethereum’s settlement layer. Prediction positions become collateral in a two-sided lending market where borrowers unlock liquidity and lenders earn yield.

These layers aren’t in tension. They’re complementary parts of the same capital efficiency stack. The exchange provides the trading and settlement foundation. Protocol-level lending extends the utility of the assets that trade on it.

What HIP-4 Brings to the Table

HIP-4 introduces outcome trading as a native HyperCore primitive. Outcomes are fully collateralized contracts that settle within a fixed range — essentially prediction market positions baked into the L1. They bring non-linearity, dated contracts, and a derivative form that composes naturally with Hyperliquid’s existing primitives.

The design is genuinely interesting. Portfolio margin, spot, and the HyperEVM all live in the same ecosystem, which opens the door to a unified trading experience where outcome exposure and perpetual exposure coexist in one account. For traders already inside the Hyperliquid ecosystem, this is a powerful proposition — no wrapping, no bridging, no external protocol dependency for the core trading experience.

In traditional portfolio margining, correlated position netting reduces collateral requirements by 30–50%. For a trader with a $100K perp book and a $50K prediction book, that’s the difference between posting $150K across two platforms versus roughly $110K–120K in one unified account. That $30K–40K freed up is capital they can actually deploy.

For the ~2,000 dual-platform whale wallets we identified, the value of consolidation is clear. These traders are already running sophisticated strategies across siloed platforms. A unified margin account is a natural improvement.

Protocol-Layer Lending as an Extension

While exchange-level margin optimizes collateral requirements for active traders, protocol-layer lending opens a different dimension of capital efficiency — one built around yield, composability, and cross-platform access.

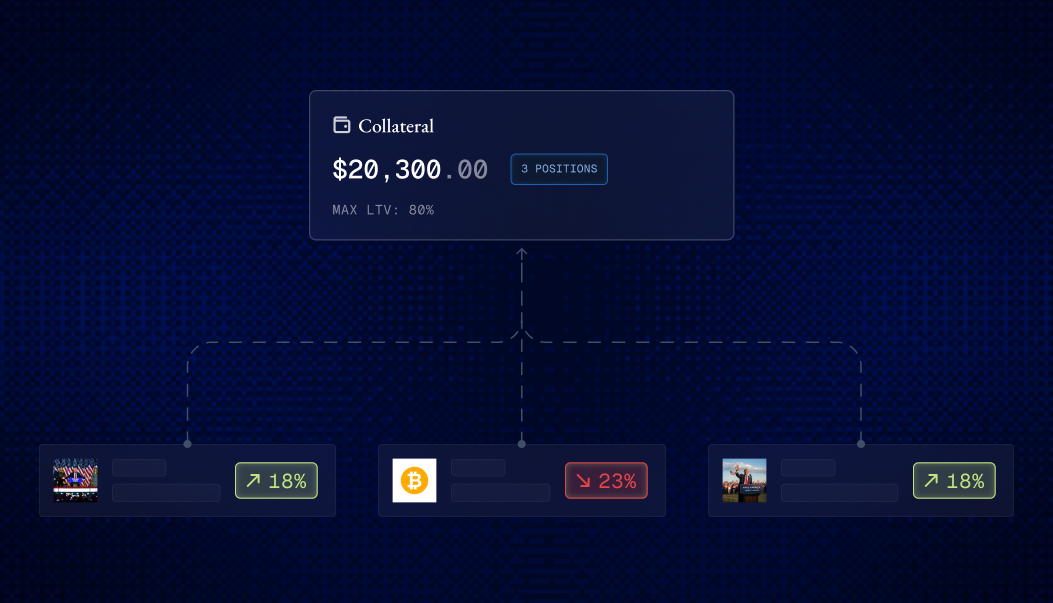

Varla’s architecture creates a two-sided market around prediction market positions. On one side, traders deposit positions as cross-margin collateral and borrow stablecoins against them — unlocking liquidity without closing their exposure. On the other, stablecoin holders supply USDC and earn yield generated by borrowing demand.

The lending protocol brings capabilities that naturally extend the ecosystem:

Yield generation. Borrowing demand from prediction market traders creates real interest income for stablecoin suppliers. This transforms prediction market activity into a yield source for the broader DeFi ecosystem.

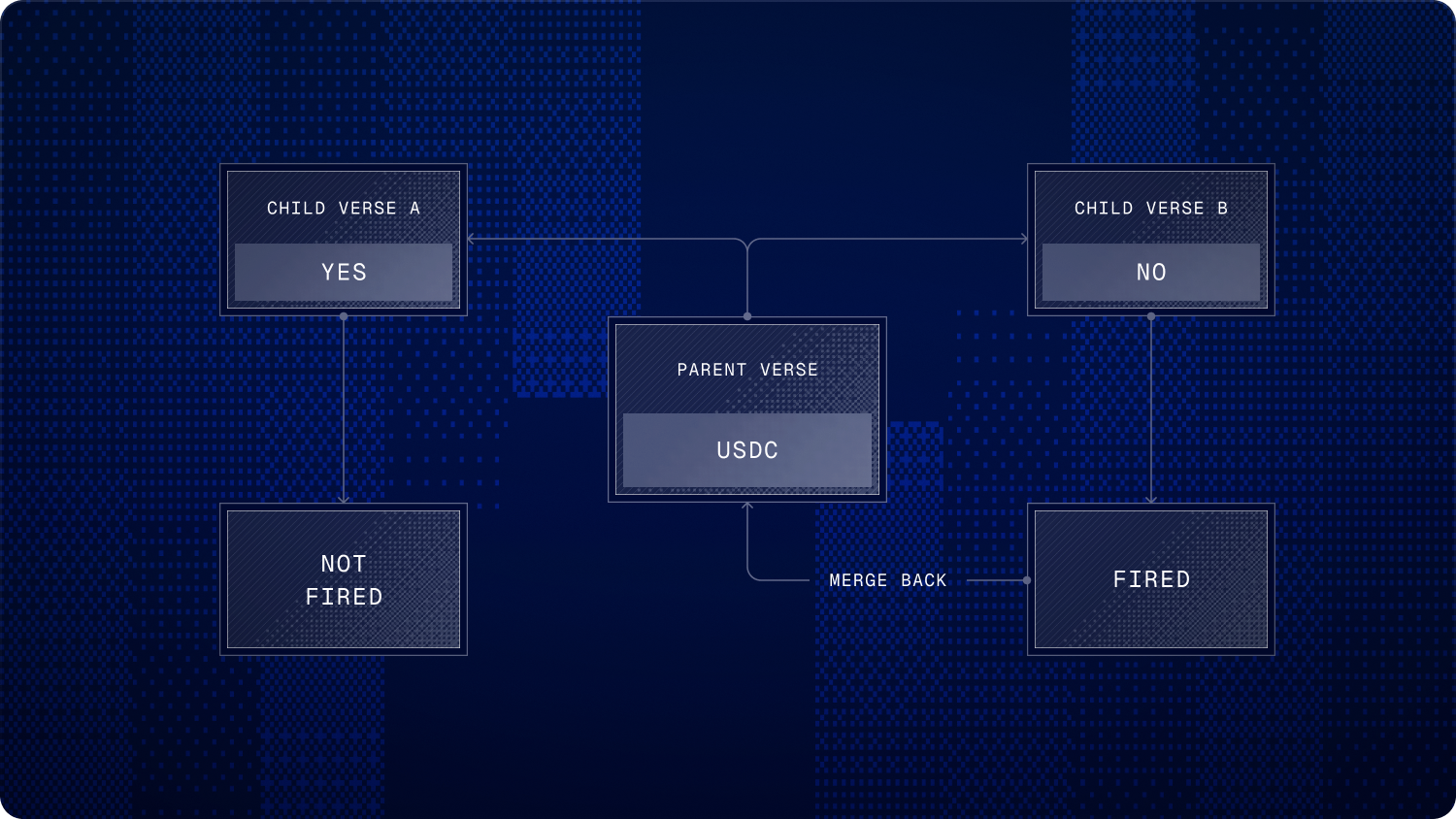

Cross-platform collateral. Varla’s adapter architecture abstracts platform-specific mechanics — handling Polymarket’s conditional token merges on Polygon, Opinion Protocol’s execution engine on BSC, and future platforms through dedicated integration layers. Positions from multiple platforms can contribute to one lending portfolio.

Purpose-built risk infrastructure. Prediction market positions have properties unlike any other DeFi collateral: bounded payoffs (0 or 1), known resolution dates, thin and episodic liquidity, and sudden settlement events. Varla’s risk engine is designed specifically for these characteristics — with tiered LTV, early-closure decay that reduces borrowing power as markets approach resolution, automatic liquidity monitoring with per-tier grace periods, and liquidation modes that understand binary merging and NegRisk conversion.

Composability. Borrowing stablecoins against prediction positions opens pathways beyond trading — yield farming, expenses, deployment into other protocols. The capital becomes productive in ways that go beyond margin optimization.

Varla on HyperEVM

Varla’s adapter pattern is designed to extend to new platforms as they emerge. Hyperliquid’s HyperEVM is a natural fit.

When Varla deploys on HyperEVM, HIP-4 outcome positions become eligible collateral alongside Polymarket and Opinion Protocol positions. Traders in the Hyperliquid ecosystem get lending infrastructure native to their chain. Stablecoin holders get a new source of yield. And the same risk engine — tiered LTV, oracle infrastructure, early-closure mechanics, merge-assisted liquidation — wraps HIP-4 positions in the same infrastructure that already serves other platforms.

The result is a stack where exchange-level margin and protocol-level lending work together. A trader can hold HIP-4 outcome positions natively margined within Hyperliquid’s matching engine and separately borrow against them via Varla for liquidity or yield — they’re independent layers serving different purposes.

The Multi-Platform Picture

The prediction market ecosystem is expanding across platforms and chains. Polymarket on Polygon. Kalshi exploring tokenization on Solana. Opinion Protocol on BSC. HIP-4 on Hyperliquid. Each platform serves different markets, different user bases, and different trading experiences.

What’s consistent across all of them is that prediction market positions — wherever they’re issued — share the same fundamental properties: bounded payoffs, known resolution dates, variable liquidity, and binary settlement. The lending infrastructure that serves this asset class needs to understand those properties at a deep level, regardless of which platform issued the token.

That’s what Varla’s adapter architecture is built for. New platforms plug into the same lending stack — the same risk engine, the same oracle infrastructure, the same liquidation logic — without rebuilding from scratch. The risk parameters adapt to each platform’s mechanics, but the core lending protocol stays unified.

For traders operating across multiple platforms, this means one lending protocol that understands their positions wherever they hold them. For stablecoin lenders, it means a single vault where yield is generated by borrowing demand from the entire prediction market ecosystem — not just one platform.

Where We’re Going

Capital efficiency for prediction markets isn’t a feature of one platform. It’s infrastructure that the entire ecosystem needs, and it’s being built across multiple layers simultaneously.

At the exchange level, Hyperliquid is bringing outcome trading and portfolio margin natively into the fastest-growing derivatives platform in crypto. At the protocol level, Varla is building the lending layer that makes prediction market positions productive — across platforms, across chains, with risk infrastructure purpose-built for the asset class.

The convergence is the point. The more platforms that issue prediction market positions, the more capital sits in those positions, and the more valuable it becomes to have lending infrastructure that makes all of it productive. The dead capital problem is real — we’ve seen it in the data. The ecosystem building around it is what solves it.