Prediction markets have product-market fit. Total open interest across the major platforms is approaching $1 billion — Kalshi at $522M, Polymarket at $448M, and growing. The demand for event-driven exposure is real and accelerating.

But the capital behind those positions is fundamentally unproductive. You can’t earn yield on it. You can’t use it as margin. You can’t borrow against it. Every dollar sitting in a prediction market position is a dollar doing nothing else — for weeks or months at a time.

This isn’t a minor inefficiency. It’s a structural problem that limits how much capital sophisticated traders are willing to commit, and it’s the single biggest constraint on the category’s growth.

The dead capital problem

In the rest of DeFi, capital is expected to work. ETH earns staking yield. Stablecoins earn lending yield. LP tokens compose with other protocols. Even NFTs have lending markets now.

Prediction market positions have none of this. When you buy a YES token for $0.65 on a market that resolves in 90 days, that $0.65 sits in a contract doing nothing for three months. No yield. No composability. No secondary utility.

The numbers are striking. On Polymarket alone, more than half of open interest is locked in markets that won’t resolve for over 30 days. $155 million is locked for more than a year. Scale that to $1 billion across platforms and the picture is clear: hundreds of millions in capital that could be earning 5-10% annualized yield in any stablecoin lending market — sitting idle, waiting for a binary outcome.

For retail traders making small bets, this doesn’t matter much. But for the sophisticated participants who drive the majority of volume — the traders running leveraged perpetual books alongside their prediction positions — every idle dollar has a real opportunity cost.

Fragmented liquidity across platforms

The capital efficiency problem is compounded by fragmentation. Prediction market liquidity is split across multiple platforms on multiple chains:

- Polymarket on Polygon

- Kalshi on Solana (via DFlow tokenization)

- Opinion Protocol on BSC

- HIP-4 (coming) on Hyperliquid

Each platform is its own capital silo. Positions don’t compose across chains. A trader with $50K on Polymarket and $100K in perps on Hyperliquid has to post $150K in total collateral — two separate pools of capital that can’t offset each other.

Research tracking ~15,000 of Polymarket’s top traders revealed that roughly 14% are simultaneously active on Hyperliquid, running $189M in perp notional alongside their prediction positions. Their Hyperliquid books are sophisticated — nearly balanced (54% long, 46% short), using an average of 7x leverage. These aren’t gamblers. They’re capital allocators running parallel strategies across siloed platforms.

The cost of that silo? $18.3 million in open prediction market positions that can’t be used as margin, can’t offset risk, and can’t earn yield. At 7x leverage, that’s roughly $128 million in trades they’re not making.

Why nobody built the lending layer until now

Prediction market positions are unusual collateral. They don’t behave like ETH, stablecoins, or LP tokens. Building a lending protocol for them requires solving problems that standard DeFi lending protocols were never designed for:

Bounded payoff. Every position pays out between $0.00 and $1.00. This is actually simpler than most collateral — the downside is capped — but standard oracle infrastructure doesn’t handle this price range or settlement mechanic.

Dated expiry. Every market has a resolution date. Collateral that expires in 2 days has a fundamentally different risk profile than collateral that expires in 6 months. No existing lending protocol has time-to-expiry as a risk parameter.

ERC1155 token standard. Aave and Compound are built for ERC20 tokens. Prediction market positions are ERC1155 (multi-token standard), where each positionId represents a different outcome. The accounting is different at the contract level.

Binary and multi-outcome structure. Some markets are simple YES/NO. Others have 8+ outcomes (NegRisk markets). Liquidation can’t just “sell collateral on a DEX” — it needs to understand binary merging (YES + NO → USDC) and NegRisk conversion.

Thin and variable liquidity. Prediction market orderbooks can range from $500K deep to nearly empty, and liquidity can evaporate as a market approaches resolution or loses public interest. The risk model needs to respond to this in real time.

Early approaches have been partial — bolt-on lending vaults that treat prediction positions like generic ERC20 collateral, perps platforms that added prediction features as an afterthought, tokenization initiatives without any collateral or lending integration. None of them addressed the full stack: PM-specific oracle, time-decay risk parameters, cross-margin accounting, and liquidation modes that understand binary and multi-outcome structures.

The gap isn’t a product gap. It’s an infrastructure gap.

How Varla’s lending pool solves this

Varla’s approach is to build the lending layer from scratch, purpose-built for prediction market collateral.

The system has two sides:

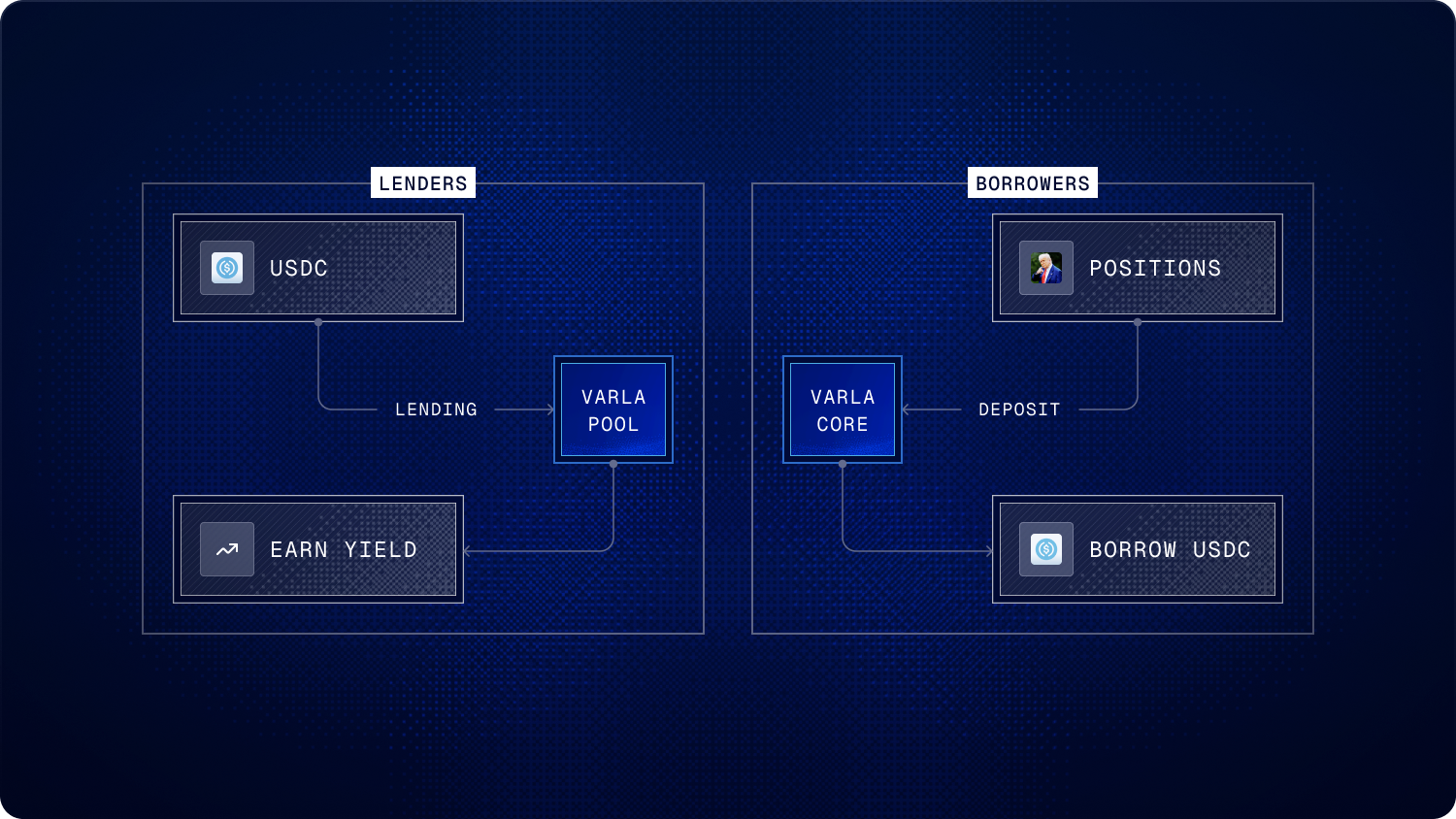

For lenders: VarlaPool is an ERC4626 stablecoin vault. You deposit USDC, receive vUSDC shares that represent your pro-rata claim on pool assets. Your yield comes directly from borrower interest — not from token emissions, not from points programs. When borrowing demand is high, rates are high. When it’s low, rates adjust automatically.

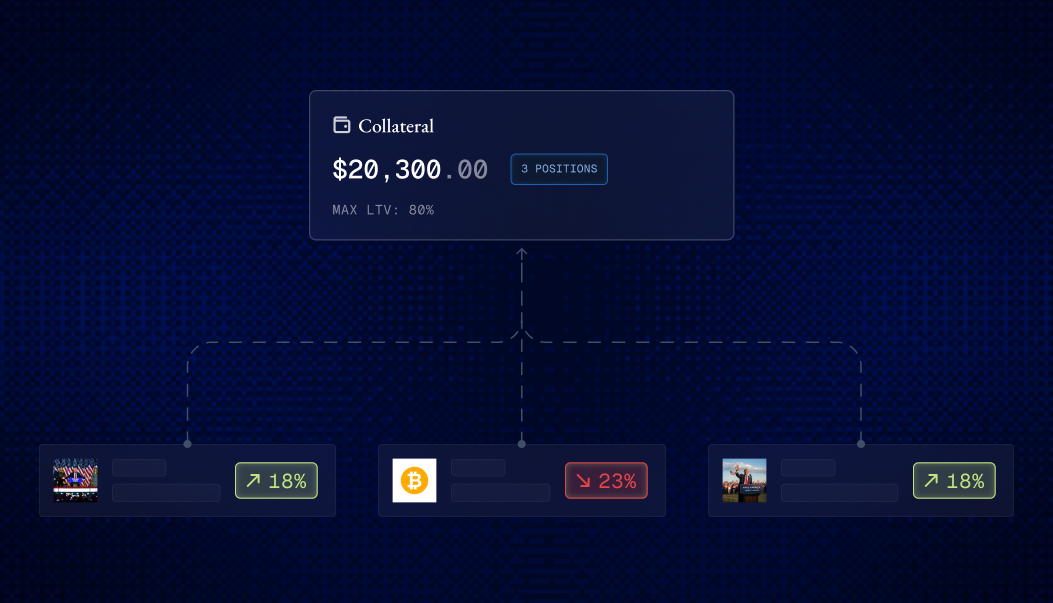

For borrowers: VarlaCore lets you deposit prediction market positions (ERC1155) as cross-margin collateral and borrow USDC against them. Your borrowing power is computed across your entire portfolio, with tiered LTV (80%/65%/50%) based on market risk.

The interest rate model uses a kinked curve — the same design pattern used by Aave and Compound, but tuned for prediction market dynamics:

- Below 80% utilization: rates climb gradually (base 2% + slope of 7.5%)

- Above 80% utilization: rates spike sharply (slope of 100%) to incentivize repayment and attract new deposits

This creates a self-regulating market. When the pool is underutilized, borrowing is cheap — attracting prediction traders who want leverage. When utilization is high, rates rise — attracting lenders who want yield. The equilibrium emerges from supply and demand.

The pool also maintains a 10% protocol reserve — a portion of all interest earned is set aside as first-loss capital to absorb bad debt before it hits lenders. This is a structural protection that doesn’t exist in bolt-on lending solutions.

Liquidation that understands prediction markets

Standard DeFi liquidation assumes you can sell seized collateral on a DEX. For ERC1155 prediction market positions, that assumption breaks down. There’s no Uniswap pool for “Will the Fed cut rates in September? — YES.”

Varla solves this with three purpose-built liquidation modes:

Simple liquidation. The most common mode. A liquidator repays some of the borrower’s debt and receives ERC1155 collateral at a bonus (5-15%, variable based on how underwater the position is). The liquidator then handles disposition of the tokens off-chain. This works for liquid markets where the liquidator has a strategy for the tokens.

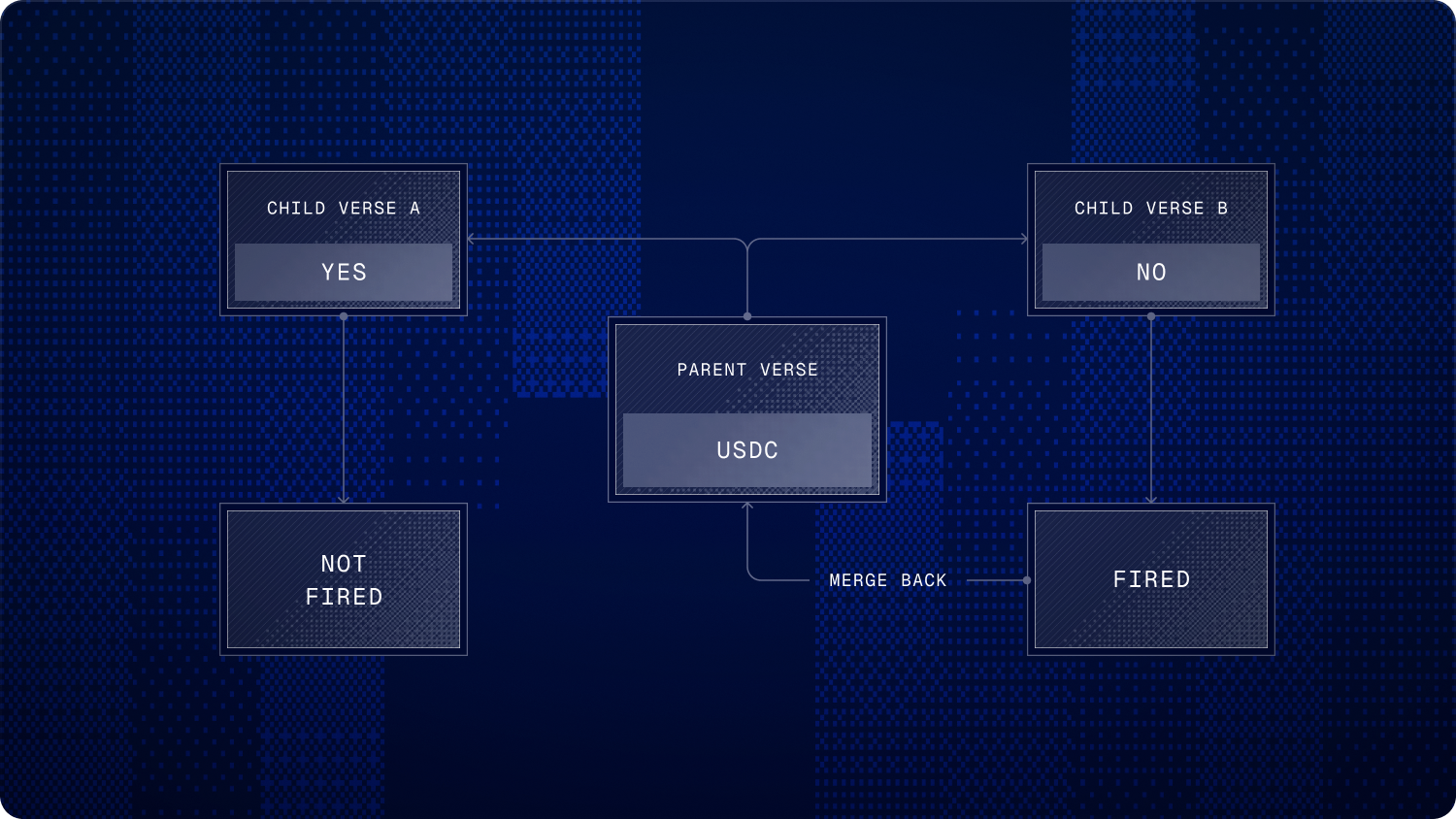

Merge-assisted liquidation. For binary markets, if a liquidator holds or can acquire the opposite side of a position, they can merge YES + NO tokens back into the underlying collateral (USDC) via the Gnosis CTF. This is handled through Varla’s platform adapters — the liquidator never needs to interact with the CTF directly. The merge is deterministic: 1 YES + 1 NO always equals $1.00.

Convert-assisted liquidation. For multi-outcome NegRisk markets, NO tokens can be converted back into collateral via the NegRisk adapter. This is the equivalent of merge for markets with more than two outcomes.

All three modes are permissionless — anyone can liquidate. The liquidation bonus scales with how unhealthy the position is: closer to the threshold, the bonus is lower (saving the borrower from excessive penalty). Deep underwater, the bonus is higher (incentivizing fast action to protect lenders).

When collateral value drops below total debt (bad debt), the protocol reserve absorbs losses first. If the reserve is insufficient, the remaining shortfall is socialized across lenders — their share price adjusts downward. This is transparent and automatic.

Risk infrastructure that adapts in real time

The most important difference between Varla and a generic lending protocol isn’t the vault or the interest rates — it’s the risk infrastructure.

Prediction markets don’t behave like perpetual collateral. They resolve. Their liquidity fluctuates. Their risk changes over time. Varla’s risk parameters respond to all of this:

Tiered LTV assigns different borrowing power based on market risk characteristics. A deep, long-dated election market (Conservative, 80% LTV) is treated differently from a thin, volatile niche market (Risk, 50% LTV).

Early-closure LTV decay linearly reduces borrowing power in the 7 days before a market resolves. This prevents a class of attacks where someone deposits a nearly-resolved position and borrows against it at full value.

Low-liquidity LTV decay monitors orderbook depth in real time. If a market’s liquidity drops below $10,000, a tier-specific grace period begins (24h for Conservative, 12h for Moderate, 6h for Risk). If liquidity doesn’t recover, LTV decays linearly to zero over 48 hours.

Oracle grace periods prevent unfair liquidations. When the oracle recovers from a stale gap, there’s a 5-minute grace window before liquidators can act — giving users time to add collateral or repay debt.

Manual invalidation gives governance an emergency kill switch. If something goes fundamentally wrong with a market (disputed resolution, oracle compromise), positions can be frozen until the situation is resolved.

None of this exists in bolt-on lending solutions. It can’t — because it requires the oracle, the risk engine, and the liquidation system to be designed together from the ground up.

Infrastructure unlocks, liquidity follows

There’s a pattern emerging across DeFi: when real infrastructure arrives, capital consolidates fast.

HIP-3 on Hyperliquid is the most recent example. When spot trading launched in late 2025, open interest went from under $200M to $1.26B in a few months. Daily volume hit $5.9B. The first serious deployer captured 85% of all HIP-3 volume — over $110B in cumulative trading in five months. Infrastructure didn’t gradually attract liquidity. It snapped it into place.

HIP-4 sets up the same dynamic for prediction markets, but with a larger addressable market. Robinhood’s Q4 2025 earnings showed ~$435M in annualized prediction market revenue — a 32% conversion rate against their other trading products. Applied to Hyperliquid’s $962M revenue base, even conservative estimates put HIP-4 prediction markets at a $130–290M annual revenue opportunity. For context, that base case is already larger than Polymarket’s and Kalshi’s estimated annual revenues individually.

The capital is ready. The infrastructure is arriving. What’s still missing is the layer that makes the capital inside these markets productive — not just for trading, but for lending, yield, and composability across the broader DeFi stack.

What comes next

The prediction market category is expanding across platforms and chains — Polymarket, Kalshi, Opinion Protocol, and soon HIP-4 on Hyperliquid. But growth in prediction market volume without growth in prediction market infrastructure just means more dead capital.

The next phase isn’t about more terminals or alternative frontends. It’s about making the capital inside prediction markets productive — for borrowers who want liquidity, for lenders who want yield, and for the ecosystem that needs deeper participation.

Purpose-built lending infrastructure that understands positions, resolution dates, liquidity dynamics, and risk tiers is the missing primitive. That’s what Varla is after.